Find out how the 2026 Budget affects your investments & structuring decisions

The detailed rules behind the Budget have not been released and remain subject to change. This article speculates about a likely outcome based on what has been announced publicly—it is general information only, not tax law advice.

The Top Level

What do you need to do immediately? Likely nothing

The rules could change again, and you have until 2028 before the 30% floor is expected to take effect. Continue to distribute to your bucket company and wait for the final legislation to pass. With what we know so far:

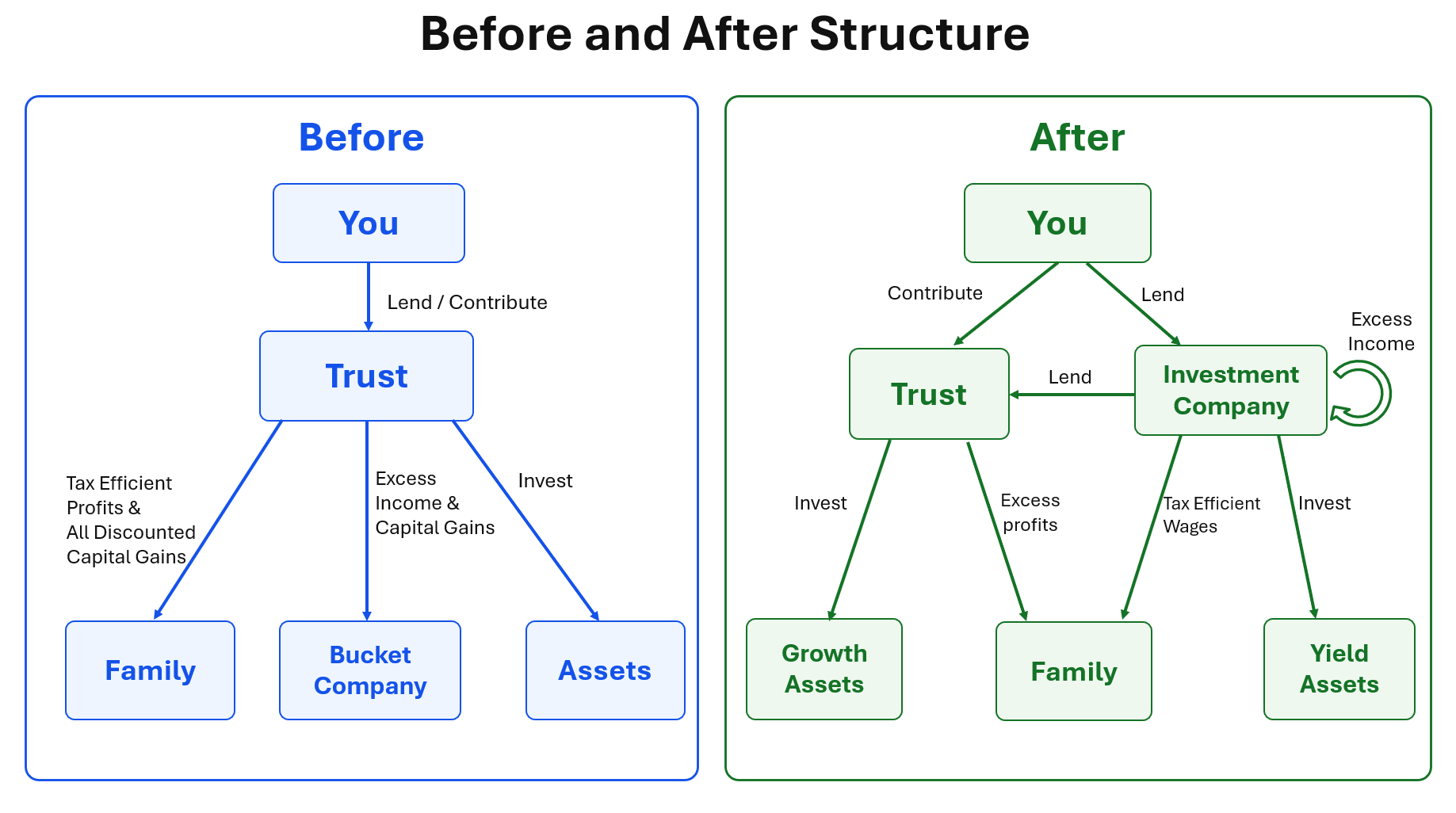

- Trusts still remain the primary instrument of protection and income distribution

- Bucket companies are no more, and will switch to being investment companies.

- Wages and Loans will be used to move low tax income rather than trust distributions. Trust distributions remain in use for >30% Tax distributions.

How the changes will be rolled out:

- May 2026 — Negative gearing for new purchases of existing properties is no longer possible; losses instead are carried forward to later years.

- Jul 2026 — Company loss carry-back for small businesses to offset gains in the previous two years.

- Jul 2027 — Capital gains for individuals and trusts will move from 50% discount to indexation with inflation and will be taxed at least 30% non-refundable (no change to companies).

- Jul 2028 — All family trust distributions will be taxed at least 30% non-refundable. Bucket companies don't receive those credits at all, so will pay double (30% + 30%) tax on any distributions received.

Although it seemed like bad news for trusts and investors, the reality is it's not a massive change at all. When the right structure is put in place the outcomes are overall the same; however, they are a little more complicated to implement.

Change 1: May 2026 — Negative gearing

The inability to negative gear will affect some investors. In practice, most investment properties are only meaningfully negatively geared for the first few years (roughly the first five), and for many holdings the gearing effect on annual taxable income is small.

New builds with large depreciation schedules are more likely to be negatively geared on paper. As commonly reported for the budget package, that kind of stock is often carved out or exempt from the same restriction on established property—subject to final legislation.

New build: Construction on vacant land, buying off the plan, subdivision / duplex developments, any of these if occupied for less than 12 months.

Not a new build: Granny flats, knock-down rebuilds, renovations.

Instead of lossing being able to reduce tax payable on other income they will instead become losses carried forwad. Over a long hold, the “lost” benefit from missing early-year refunds can be much smaller than it feels in year one: instead of tax refunds in years 1–5 then tax on profits from year 6, you will see no refunds and no tax in years 1–10, because losses from years 1–5 absorb income in years 6–10. The tax timing shifts; the cumulative position is the same.

It should be noted that all other asset classes can still be negatively geared, it's just property which this loop hole is closing. Debt recylcing remains a useful tool to negatively gear with as long as it is used to purchase non-property assets.If you are impacted, a response is debt recycling on the investment-property loan so the property is no longer negatively geared: the loan purpose is traced to new use (for example capital contributed or lent onward to your investment company to fund other investments), so interest is no longer framed as a deduction against that rental property in the same way.

With the right planning in place the negative gearing change will:

- Only impact you if you're fully leveraged with no spare cash to debt recycle

- Only impact recently purchased property assets

- Have minimal to no long-term effect, as the losses carry forward.

Due to misunderstanding it is likely to reduce the value of property in the short term as investors become spooked. As Warren Buffett put it, “Be greedy when others are fearful.”

Change 2: Jul 2026 — Carry-back losses

Currently losses can only be carried forward to offset later year gains; you can't have a loss this year, and then ask for the tax back you paid last year. This change allows small business to carry back losses up to 2 years.

Your bucket company is currently paying tax on all the excess income of the trust. If in 2028 you start having expenses in the company (such as wages or interest on loans) that exceed the company's income because you can no longer distribute to bucket companies, you may be able to recoup past-year tax payments under the carry-back rules.

Another way of thinking about it is instead of having to pay tax on the profit you make in each financial year, you can look at the average profit over a three-year period.

Farmers already have this exact ability for primary production gains over a five-year period; this change is just expanding it to all small businesses.

Example

Your bucket company — now repurposed as your investment company — makes $100,000 profit in 2027 and pays $30,000 tax. The same in 2028: another $30,000 tax paid. In 2029 you have moved investments around and the company records an $80,000 loss. It makes no profit for the next 5 years, then makes another $100k profit

What happens to the $80,000 loss?

Old rules: The loss sits in the company waiting for a future profit year. 5 years later instead of paying $30k it pays $6k in tax as the loss covers the $24k

New rules (carry-back): You apply it back against 2028's profit. The ATO refunds $24,000 (30% of $80,000) of the tax you paid in 2028. You can then invest that $24k which previously the government held onto

With the right planning in place the carry-back losses change will:

- Make tax planning a bit easier, as the averaging means you don't need to get it perfect every year

- Effectively delay tax payments so you have more to invest with

Change 3: Jul 2027 — Capital gains indexation

From Jul 2027 all assets, no matter when they were purchased, will use indexation of cost base to determine taxable capital gain—even assets purchased prior to 1984, which previously did not have to pay any CGT. The only exemption is purchasing a newly built property, which can choose between the discounted or indexed method.

Similar to how the cost base at first income generation works for your principal place of residence, when you have an asset that was purchased before the new rule comes into effect you can choose to apply the transition from old to new method either by time or by value.

Say you held an asset for 10 years, 5 years before and 5 years after the change. If the asset grew by 10% p.a. starting from $100 it would have grown $61 in the first 5 years and $98 in the last 5 years ($159 in total). You have the choice to be taxed using the growth based on the value at the time ($61 vs $98), or you can time-apportion it half each ($79 vs $79). You don't need to make that decision until you sell the asset, but you do get to pick the better of two options, and the lower-tax option will depend on what the inflation rate was during the last 5 years.

Discount vs indexation

Starting value and original cost base $100. The lines show how the asset value, cost base, indexed cost base, and the 50% discount path evolve over ten years. The columns show how a single sale in year 10 splits into taxable gain, tax-free gain, and return of capital. Notice how if inflation is greater than growth you pay no tax, if growth is more than double inflation you pay more tax.

Investment growth and inflation

- Asset value

- Cost base

- Indexed cost base

- 50% discount

- Taxable gain

- Tax-free gain

- Return of capital

With the right planning in place the capital gains indexation change will:

- Reduce the tax on average investments like Australian stocks and Australian property

- Increase the tax on high-growth investments like US tech stocks

- Make holding companies useful for very high-growth investments (for example starting a business you plan to sell in five years for millions)

- Require more planning in asset choice to ensure you utilise the low tax thresholds with wages or yield returns

- Have no impact on principal place of residence CGT exemption

- Have to keep more records for determining capital gains

Change 4: Jul 2028 — 30% tax on trust distributions

This 30% minimum tax will be classed as a non-refundable tax offset. This is the same as how the foreign income tax credit is classified currently, but different to franking credits, which are a refundable tax credit.

This change has no impact on you if you have other income such that you are over the 30% marginal tax bracket.

So all you need to do is have your own income (from working, investments, and so on) that gets you and each of your family members over the $45k bracket.

- If you have a job, you are likely already there.

- If you do not mind working, you could work for your investment company a few hours a week and pay yourself a modest wage of $50k.

- If you do not have a job and do not want to work, you could loan your investment company or trust $500k and charge 10% interest.

Bucket companies do not receive the tax credit at all. This means that if the trust has $100 to distribute, the trust has to pay $30 in tax, and then distribute the $70. When the company records its income it declares the $70 and then has to pay the company tax rate on that of 30% ($21), leaving you with $49—effectively a 51% tax rate and only 21% retained as franking credits.

Conversely, for individuals: if you were in the 47% bracket the $70 would be distributed to you with the $30 non-refundable credit. You would have to pay 47% tax on the total $100, leaving you with $53 post-tax.

Because of the capital gains discount, and now indexation, a 5% p.a. growth asset produces about the same take-home profit over the years as a 7% yield asset. This is simply because you get to “reinvest” the 5% growth return each year without getting taxed.

Before, if you had the choice of a guaranteed 10% growth or guaranteed 10% yield asset, you would invest all your money in the 10% growth.

With growth assets now being taxed at 30% no matter what bracket you are in, you need a little bit of yield/income in your income to use up the $45k lower tax brackets.

The good news is shares already have a mix of yield (dividends) and growth, so they already do exactly the split you are after. The tax minimisation goal is getting the money out of the family trust without it being classified as a distribution.

Example

$100,000 of trust income, spouse on individual rates (tax-free threshold plus 16% / 30% brackets — roughly $22,000 tax on $100,000).

| Scenario | Description | Post-tax |

|---|---|---|

| Current rules | Distribute $100,000 to your spouse. She pays tax at individual rates — roughly $22,000. Net to the family: $78,000. | $78,000 |

| New rules (from Jul 2028) | ||

| Option 1 - Do nothing | The trust pays $30,000 tax first. Your spouse receives $70,000 with a $30,000 non-refundable credit. Her tax on $100,000 at individual rates is still ~$22,000, but the credit only offsets tax owed — she does not get the ~$8,000 difference refunded. | $70,000 (−$8,000) |

| Option 2 - Spouse loan | Withdraw capital from the trust; your spouse lends it back to the trust. The trust pays her $100,000 interest (deductible to the trust; taxable to her at individual rates). | $78,000 |

| Option 3 - Spouse works | The investment company lends to the family trust at the Division 7A rate. The trust pays $100,000 interest to the investment company; the company pays a wage to your spouse. She pays tax at individual rates on the wage. | $78,000 |

With the right planning in place the July 2028 trust distribution changes will:

- Have no impact on your total tax paid

- Reduce asset protection as more funds need to stay in individuals' names as loans

- Require more planning to set up loans between entities to utilise low marginal tax rates without distributions

- Have a minor impact on asset choice to ensure there is enough income generation to cover the low tax brackets of all family members

Planning: Structure & assets holder

Because we cannot distribute income to a bucket company to avoid paying the 40%+ tax, and allowing franking credits to be retain, we need a different way to do this. The solution is to invest from the bucket company directly (repurposed as the investment company) .

However companies can't take advantage of the indexaction to reduce capital gains, so any asset that produces a capital gains should stay in trust, unless that gain is so large that it's effectively income becuase the indexaction discount has virtually no impact (or inflation is zero).

As we therefore will have investments in the trust we want a way to expense the income generated by those investments instead of having to distribute them, which can be done via a loan to the trust moving the income back to the bucket company.

Simiarly because we can't use trust distributions to utilise low tax thresholds, we need to use other means to expense the income from the trust or investment company to individuals, which can be done via loans or wages.

As a result we're making structural and asset holder changes to achieve the exact same benefits which trusts currently give us:

- Retaining earnings in the bucket company via interest payments instead of distributions.

- Utilising low tax brackets via wages or interest payments instead of distributions.

- In general, holding yielding assets in your company and growth assets in your trust.

Growth vs yield assets

Growth assets (typically held in the family trust): shares, property, gold — assets whose value tends to rise by roughly 1–30% p.a. and that you intend to sell to realise a capital gain. Companies cannot use indexation on capital gains, so moderate-growth assets stay in the trust.

Yield assets (typically held in the investment company): loans, bonds, small businesses you plan to wind up, and very high-growth businesses (above about 30% p.a.) where the gain is so large that indexation offers little benefit — treated on the yield side for structuring even when growth is extreme.

Shares often combine both: dividends (yield) and price growth (capital gain), which is why a balanced portfolio can still split cleanly between trust and company once you classify each holding.

First, put enough capital into the investment company so that its income can cover required wages (and related running costs) without starving the portfolio.

Income-heavy investments tend to look better inside an investment company, because company tax on income is lower (30%) than personal tax (47%) on trust distributions.

For a typical balanced holding in the rough ballpark of about 4% growth and 4% income, trusts not only remain the preferable asset holder, but you are actually better off vs the current discounting method.

Post tax return vs current, and which structure to use

- Hold Asset in Trust & Better off by %

- Hold Assets in Trust & Worse off by %

- Hold Assets in Company

The horizontal axis is growth % p.a.; the vertical axis is income % p.a. Shading shows which side delivers higher after-tax cash in a simple model (47% marginal rate, 3% inflation). The lines indicate how much better or worse your after-tax position is after 10 years compared with the current method.

What do you need to do?

Nothing yet. The rules could change again, and you have until 2028 before the 30% floor is expected to take effect.

If these rules go ahead substantially as announced, a plausible sequence would be:

- Before the new rules apply, sell the yield-only assets in the trust (private credit, some bonds).

- Distribute the last bits of discounted capital gains to family members, and stream remaining income to the bucket company.

- Re-purpose the bucket company as your yield-only investment company, carrying forward its existing franking credits.

- Ensure your investment company has enough income to cover all family members' <30% income brackets as wages or interest on lending. If there is excess Division 7A capacity, lend it to the family trust.

- Use the investment company for: (1) yield-only assets, (2) assets you never intend on selling, (3) assets that may grow faster than about 30% p.a.

- Contribute any excess capital you want protected back into the trust for asset protection.

- Continue to use your trust for growth investments.

Example

If you had $1m to invest with and no longer worked.

You would lend $450k to your family trust at 10% p.a., delivering your $45k in the low tax brackets from the family trust.

You would contribute the remaining $550k to the trust. Together the million could be invested into a variety of assets delivering 4.5% yield and 5.5% growth (shares plus a little bit of bonds or lending).

The $45k payment to you is an expense for the trust, offsetting the 4.5% on $1m invested completely. Until you sell the assets the trust would record no income and no capital gain to distribute.

Compared to today there is no tax difference, only an asset protection difference—as previously you would have contributed the full $1m to the trust having nothing in your name; now you have $450k in your name as a loan to the trust.

Phased transition: building the investment company

Phase 1 — Building up the investment company (before 1 July 2027)

- Distribute trust earnings to the bucket company (while that still works under current rules).

- Decide how much you are willing to hold in the company for: (a) yield-only assets, (b) assets you never intend to sell, and (c) assets that may grow faster than about 30% p.a.

- Lend at zero interest personally or from the family trust to the bucket company so it can make those investments.

- Retain those earnings inside the bucket company.

Phase 2 — Switching growth back into the trust

- Sell the high-yielding assets in the investment company.

- Repay the zero-interest loan from the trust.

- Lend excess funds to the trust at the Division 7A benchmark rate.

- Invest in growth assets in the trust; use yield from those (or other trust income) to service the Division 7A loan interest and claim the deduction in the trust.

How will this impact your existing structure and fees?

| Item | Before | After |

|---|---|---|

| Typical stack | Family trust, corporate trustee, bucket company | Family trust, corporate trustee, investment company |

| Self Managed fees | $1,000 | $1,000 |

| ASIC fees | $660 | $660 |

So on a like-for-like structure (same number of companies and the same reporting load), your Self Managed and ASIC fee lines can stay in the same ballpark—the change is what each entity does with cash and investments, not necessarily how many entities you pay to register and maintain.

This article is general information only and should be tailored to your circumstances.